Strategic Leverage in a Shifting Global Order

Strategic Leverage in a Shifting Global Order

By Mehmet Enes Beşer

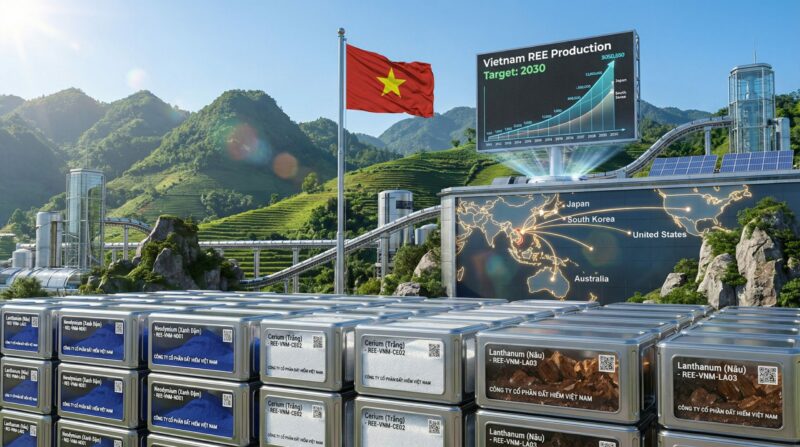

Vietnam, customary pro of sound economic policy and geopolitics three-holing, is diving into a fresh world of international scrutiny: rare earths. While the globe franticly strives to gain access to the dominant minerals found in electric vehicles and vans, windmills, and high-end electronics, Vietnam’s unexploited reserves of rare earth among the world’s best outside China are being brought to the fore. But Hanoi’s decision to expand its rare earth extraction and processing capabilities is not driven solely by economic incentives. It is also a calculated strategic move to reorganize its role in international supply chains, boost security partnerships, and hedge against geopolitical risk.

Vietnam’s deposits of rare earth, found primarily in northwest provinces such as Lai Châu and Lào Cai, are the world’s second largest, after China’s. But they have largely remained dormant due to technology, environmental, and investment constraints. That is diminishing. Vietnam has made extremely firm steps over the last several years to tap that hidden wealth. The government, in October 2023, made a brash auction of new mining rights and set out to sign deals with Western and local companies to assist in the development of its rare earth sector.

Since China controls over 80% of global rare earth processing capacity, Vietnam’s rise as a likely replacement source has geopolitical implications. Rare earths are not so much commodities in the sense of metals like copper or zinc—strategic minerals, essential to civilian industry and military technology. As U.S.-China relations grow more tense, and the EU insists on supply chain resilience, Vietnam’s rare earth sector will become a keystone in new world mineral networks.

But in the case of Vietnam, this is not just to occupy a niche market heretofore unfilled by diversification out of China. It is a means towards greater strategic autonomy. By making itself irreplaceable in the supply chains of great powers’ rare earth, Vietnam can extract maximum bargaining leverage in bilateral and multilateral forums. The policy is the natural correlate of the nation’s general style of foreign policy as “bamboo diplomacy”—subpar but solid, hedging between big power rivals without depending too greatly on any one of them.

The reasoning behind the strategy is straightforward: if Vietnam can be included in international clean technology supply chains—not just as a factory, but as a source of essential minerals—it is harder for any great power to shut it out. This is an additional layer of security at a time when the South China Sea is still a tinderbox, and regional strategic balances are fragile.

Besides, the rare earth plan is also compatible with Vietnam’s industrial policy direction and climate. Since the country is transforming to a green economy and becoming a high-tech investment center, ownership of the rare earth asset is something to negotiate for when negotiating with battery makers, clean energy producers, and electronics producers. The Vietnamese domestic technological capability can be upgraded by utilizing the rare earths if value-added processing is retained onshore and not exported abroad as raw material.

However, this belligerent strategy has its downsides. Rare earth mining is conventionally an ecologic devastator, full of poisonous wastes and radioactive threats. Vietnam will have to tread over China’s devastation of the environment in rare earth regions. Enforcing strict regulatory measures, obtaining stakeholders’ involvement, and using eco-friendly technology will be required if Hanoi is to prosper with people’s endorsement and draw green-minded investors.

Moreover, technology deficit of processing and refining remains. It’s a beginning with rare earths to mine with—a once labor actually begins at separation and purification processes—those where China has upper hand. The challenge can be filled only by a mission of technology advanced nations and companies. The recent US, Australian, Japanese, and South Korean enthusiasm also represents a preliminary willingness to invest but coordination, transparency, and regulatory certainty will play the last trump cards in making such alliances’ depth and sustainability real.

Vietnam will also need to balance the geopolitical risks of being a strategic supplier. As countries position themselves for access to the rare earth, Hanoi will need to balance competing dunes from the U.S., China, the EU, and regional players. The challenge will be how to use its rare earth bargaining chip without becoming too entangled in great power competition—a test of diplomacy as much as industrial policy.

Conclusion

Vietnam’s pursuit of developing its rare earth industry is a model of how natural resources can both drive economic progress and serve as instruments of statecraft strategy. In pursuing status as a key center of the world’s clean technology supply chain, Vietnam is not just mining minerals—it is charting a new path in an era of resource competition, technological decoupling, and multipolar geopolitics.

It won’t be because of the richness of its earth. It will require institutional overhaul, ecological husbandry, high-tech investment, and diplomatic nicety. But managed well, Vietnam’s unusual earth project may make it into a manufacturing laggard-to-be-resource-based agenda leader, one mineral at a time.